Are you looking for down payment assistance but don’t want to deal with all the red tape of typical government and grant programs? A Kansas City area bank is offering loan money that you don’t have to pay back and doesn’t require a lot of paperwork. You can use it for a qualifying home purchase or to refinance your home. You can close on your home quickly and won’t pay extra for taking this money.

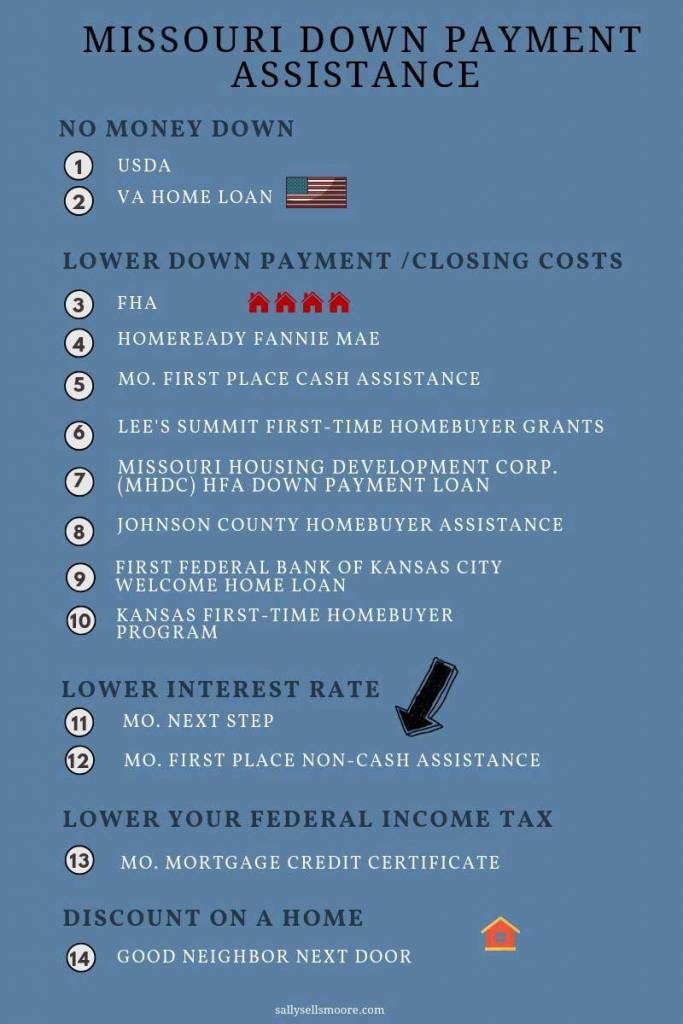

Missouri housing grants

If you’re renting right now, you could be investing your money into a home. You’ll earn equity rather than paying someone else’s mortgage.

Run the numbers for renting versus buying in this calculator comparison.

There are low-income home buying programs in Missouri, down payment assistance, and housing grants to make your dream of homeownership possible.

When you work with an experienced real estate agent, like one from the Sally Moore Real Estate Team, we’ll walk you through everything and pair you with a lender who helps first-time homebuyers and others who qualify for down payment help. That way you can find the best down payment assistance or housing grant in Missouri for your personal and financial situation.

First Federal Bank of Kansas City

With the Welcome Home Community Loan Program from First Federal Bank of Kansas City, you get $3000 for closing costs or down payment help. This low-income home buying program helps home buyers with low-to-moderate income or homeowners buying a home in a low-to-moderate census tract.

It’s not just for first-time homebuyers. You can also use the money to refinance a property or if you’ve previously bought a home.

This housing grant money has several benefits including:

- No extra hoops or paperwork.

- Purchase a home quickly.

- Don’t have to pay back the money.

- No extra fees.

- Reduced appraisal cost.

With this loan, you’ll only pay $150 for the appraisal instead of the standard $450 fee. [ Download PDF Welcome Home Loan First Federal Bank of Kansas City ]

Your loan will cost the same whether you qualify for the program or not. You can apply for the loan here.

“You shouldn’t have to throw away money renting if you can have one little boost to be a homeowner. It will put them in a way better position short term and long term,” explained Geony Rucker, a Community Loan Officer with First Federal Bank of Kansas City.

Low-income home buying program

You can use the Welcome Home loan program money to buy a home or refinance. Homebuyers qualify for homes in a low-to-moderate income census tract or low-to-moderate income.

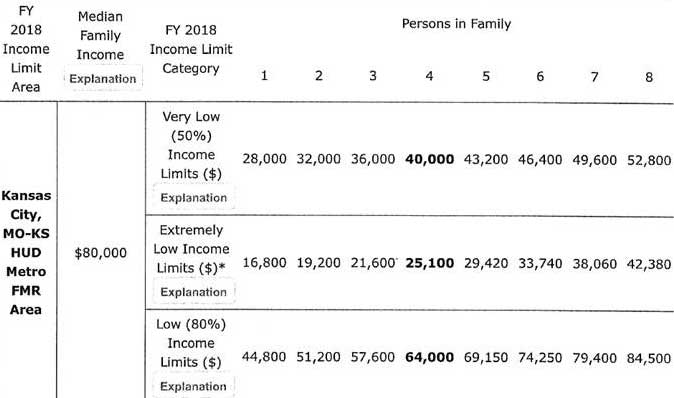

According to federal guidelines, this includes a family of four making between $25,000 and $64,000.

If you don’t meet the income guidelines, your home must be in a qualifying census tract. To find your census tract, plug in your address here. Then, compare your census tract to the guidelines for Jackson County [Download Low Income Tracts PDF]. If it’s considered “low” or “moderate” then your new home qualifies.

Remember, you only need to qualify based on income or the census tract.

“It’s an awesome program. It’s not very often that you get to get free money, let alone money where you’re not having to pay it back after you close,” explained Geony.

You can use the money however you want.

“With this, you can use it for down payment or closing costs. In a market where sellers are not wanting to pay closing costs, it’s really nice to have this as an option to help you with that,” said Rucker.

Missouri loan with less than 20% down

Missouri loan with less than 20% down

Down payment programs lower the amount of money you need to put down to close on the lown.

While 20-percent is often the gold standard, there are ways to put down less than 20-percent.

The Welcome Home Loan from First Federal Bank KC requires just a 3-percent down payment, compared with a traditional loan of 20-percent.

So, how do you qualify?

- Owner-occupied, single-family properties only.

- No minimum loan amount.

- Minimum down payment of only 3%.

- First-time homebuyers must complete an approved homebuyer education program offered by a local housing organization.

Borrowers must also receive Approve/Eligible DU Findings & meet secondary market underwriting guidelines. The underwriting system will verify that your loan meets all financial requirements and your income and assets are accurate right before closing. This is required for all loans and does not add any extra time to the loan processing.

[trx_call_to_action title=”Free Buyer’s Guide” style=”1″ accent=”no” custom=”no” link=”https://sallysellsmoore.com/home-buyers-guide/” link_caption=”Download now!”][/trx_call_to_action]

The loan is just one part of the home buying process. When you’re buying your first home, use this first-time homebuyer checklist to make sure you’re prepared for every step of the process.

VA Home Loan Benefits

Like many down payment assistance programs, there are additional benefits for Veterans. If you qualify for a VA loan, you can then combine the Welcome Home program with it. So, you can get no down payment with the VA loan and then an additional $3000 that you can use for closing costs.

“When you combine the fact that they don’t have to make a down payment with an additional $3000 in closing costs they’re coming out with very little out of pocket. So it’s an outstanding program for vets that qualify,” Rucker explained.

We believe everyone deserves to be a homeowner no matter someone’s life situation. It’s a hand up, not a hand out. You still have to qualify for the loan.

I’ve had many people cry at closings because they never thought they could buy a home. It’s hard to buy a home when you’re paying rent and have a car loan. Life is expensive. Saving $3000 is not easy to do when you don’t make a lot of money.

3751 NE Ralph Powell Road

3751 NE Ralph Powell Road